LLC vs Sole Proprietor Tax Comparator

Use our free LLC vs sole proprietor comparison tool to see the exact tax difference between both business structures based on your income. No sign-up required.

Potential annual savings with LLC

—How to use this LLC vs sole proprietor comparator

Our LLC vs sole proprietor tool gives you a side by side tax comparison in seconds. Simply enter your income details and see exactly which structure saves you more money.

Enter your annual net income — your total self-employment income after business expenses.

Select your filing status — this affects your federal income tax bracket calculations.

Enter a reasonable salary for the LLC S-Corp scenario — typically 50–60% of net income.

Hit Compare to see the tax breakdown and annual savings side by side instantly.

LLC vs sole proprietor — what is the difference?

Both LLC and sole proprietor are common business structures for US freelancers and small business owners. However, they differ significantly in terms of liability protection, tax treatment, and administrative requirements. Our LLC vs sole proprietor comparator helps you see the financial impact of each choice based on your specific income.

What is a sole proprietorship?

A sole proprietorship is the simplest and most common business structure in the US. There is no formal registration required — if you earn self-employment income without setting up any other entity, you are automatically a sole proprietor. As a result, it is the default structure for most new freelancers and 1099 workers.

However, as a sole proprietor your personal and business assets are legally the same. This means that if your business faces a lawsuit or debt, your personal savings, car, and home could be at risk.

What is an LLC?

A Limited Liability Company (LLC) is a formal business entity that separates your personal assets from your business liabilities. In other words, if your business is sued, only the business assets are at risk — not your personal ones. Furthermore, an LLC can elect to be taxed as an S-Corporation, which is where the significant tax savings come from at higher income levels.

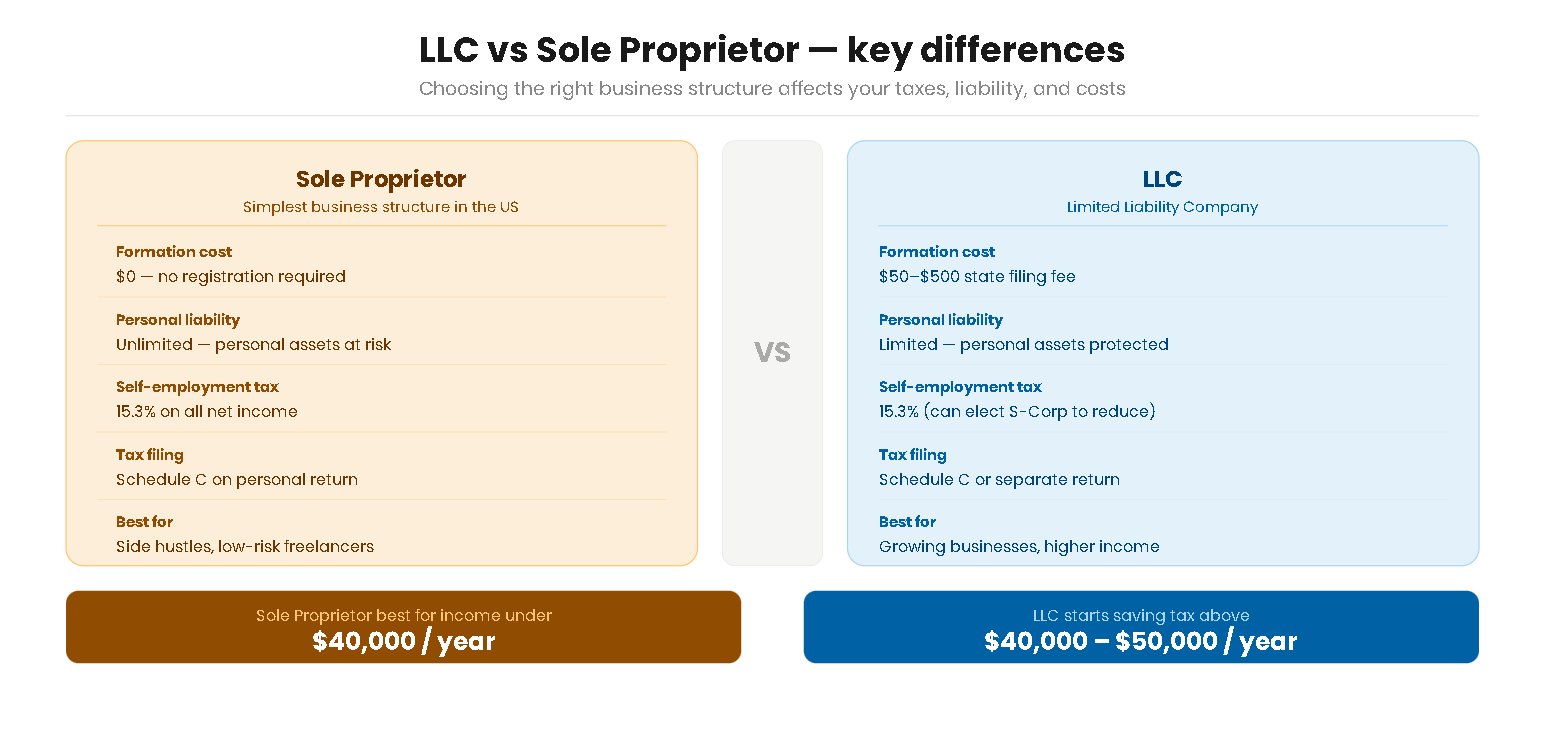

LLC vs sole proprietor — full tax comparison

The biggest financial difference between LLC and sole proprietor comes down to self-employment tax. Here is a detailed side by side breakdown of how each structure is treated by the IRS:

| Factor | Sole Proprietor | LLC (S-Corp) |

|---|---|---|

| Formation cost | $0 | $50 – $500 |

| Annual maintenance | None | $0 – $800/year |

| Personal liability | Unlimited | Limited |

| SE tax applies to | All net income | Salary only |

| SE tax rate | 15.3% | 15.3% on salary |

| Tax filing form | Schedule C | Form 1120-S |

| Payroll required | No | Yes |

| Best income range | Under $40,000 | Over $40,000 |

Key insight — with an LLC S-Corp election, you pay self-employment tax only on your salary, not on the full business profit. The remaining profit is taken as a distribution, which is not subject to SE tax. This is where the significant savings come from at higher income levels.

When should you switch from sole proprietor to LLC?

The right time to form an LLC depends on two main factors — your income level and your risk exposure. Generally speaking, most tax professionals recommend considering an LLC when your net self-employment income consistently exceeds $40,000 to $50,000 per year.

Switch to LLC if:

- Your net annual income is consistently above $40,000 – $50,000

- You work with clients in industries with higher legal risk (consulting, construction, healthcare)

- You have significant personal assets you want to protect

- You want to appear more credible and professional to larger clients

- You plan to bring on partners or investors in the future

Stay as sole proprietor if:

- Your income is below $40,000 per year — LLC costs may outweigh tax savings

- You are just starting out and testing a business idea

- Your business has low liability risk

- You want to minimize paperwork and administrative overhead

Important — forming an LLC does not automatically reduce your taxes. You must elect S-Corp tax treatment with the IRS (Form 2553) and pay yourself a reasonable salary to benefit from SE tax savings. Always consult a CPA before making this decision.

Learn more from trusted government resources:

IRS.gov — Business Structures Overview SBA.gov — Choose a Business Structure