Closing Costs Estimator

Use our free closing costs estimator to find out exactly how much you will pay at closing when buying a home in the US. Get an instant breakdown — no sign-up required.

How to use this closing costs estimator

Getting your closing cost estimate takes under a minute. Our closing costs estimator breaks everything down into clear line items so you know exactly where your money goes.

Enter the full home purchase price of the property you are buying.

Enter your down payment — the difference becomes your loan amount.

Select your loan type — conventional, FHA, VA, or USDA.

Select your US state — closing costs vary significantly by location.

What are closing costs?

Closing costs are the fees and expenses you pay on top of the purchase price when finalizing a home purchase. In other words, they are the costs associated with processing, securing, and completing your mortgage loan and property transfer.

On average, US buyers pay between 2% and 5% of the home purchase price in closing costs. Therefore, on a $350,000 home, you could expect to pay between $7,000 and $17,500 at closing — in addition to your down payment.

Who pays closing costs — buyer or seller?

In most US real estate transactions, the buyer pays the majority of closing costs. However, it is common to negotiate with the seller to cover a portion of these costs, particularly in a buyer's market. This is known as a seller concession and can significantly reduce your out-of-pocket expenses at closing.

Additionally, some lenders offer a no-closing-cost mortgage option, where the fees are rolled into your loan balance or covered in exchange for a slightly higher interest rate. As a result, you pay less upfront but more over the life of the loan.

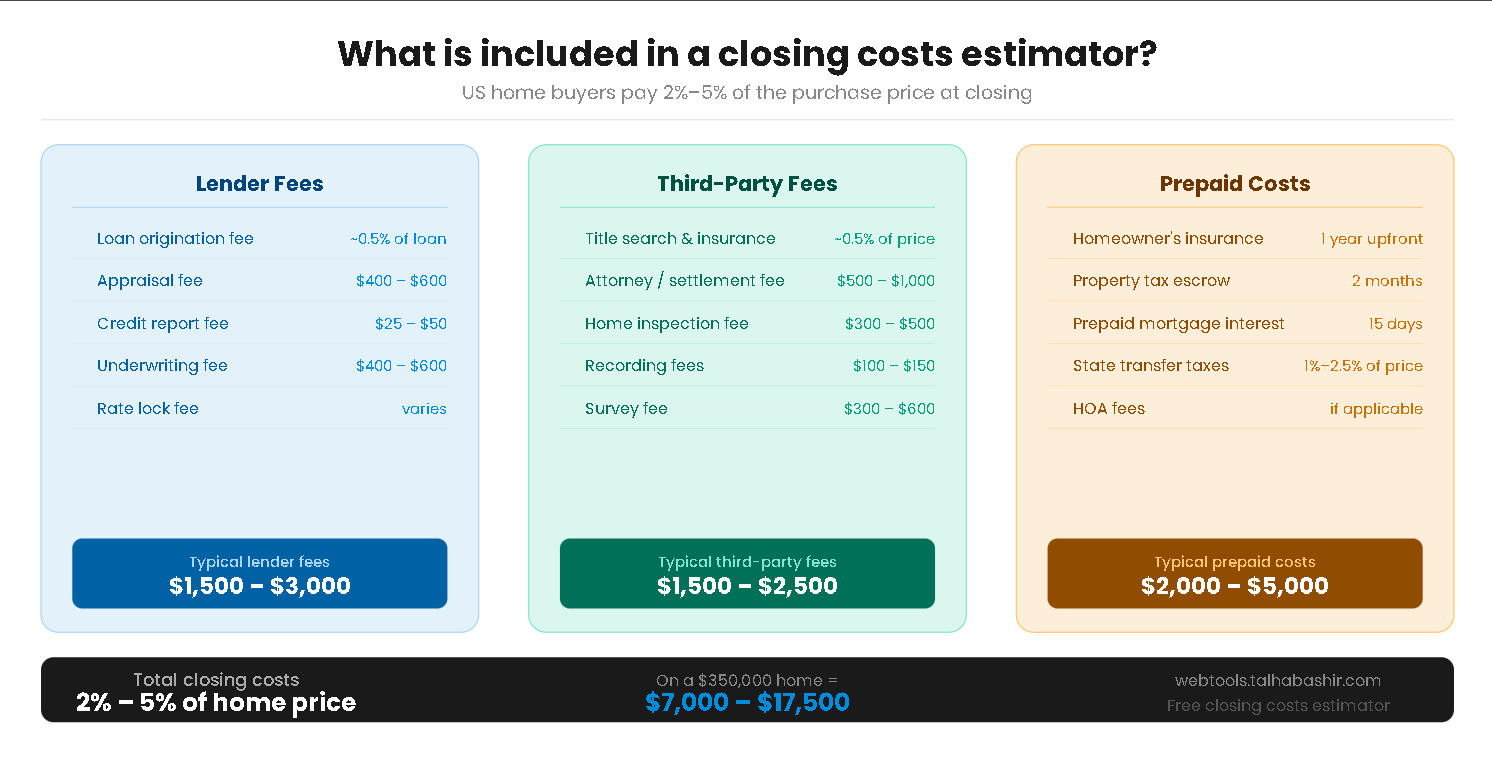

What does our closing costs estimator include?

Our closing costs estimator breaks your total costs into three main categories. Understanding each one helps you prepare financially and avoid surprises on closing day.

Lender fees

These are fees charged directly by your mortgage lender to process and approve your loan.

- Loan origination fee

- Appraisal fee

- Credit report fee

- Underwriting fee

- Rate lock fee (if applicable)

Third-party fees

These are fees paid to outside companies involved in completing the transaction.

- Title search and insurance

- Attorney or settlement fee

- Home inspection fee

- Recording fees

- Survey fee (if required)

Prepaid costs

These are upfront payments for recurring expenses collected at closing.

- Homeowner's insurance (1 year)

- Property tax escrow (2 months)

- Prepaid mortgage interest

- State transfer taxes

- HOA fees (if applicable)

Average closing costs by US state

Closing costs vary considerably across the United States, primarily due to differences in state transfer taxes and local fees. Consequently, where you buy has a major impact on your total cost at closing.

Highest closing cost states

| State | Average closing costs | % of home price |

|---|---|---|

| New York | $8,256 | 2.4% |

| Maryland | $8,750 | 2.5% |

| Massachusetts | $8,050 | 2.3% |

| Delaware | $7,700 | 2.2% |

| New Jersey | $7,700 | 2.2% |

Lowest closing cost states

| State | Average closing costs | % of home price |

|---|---|---|

| Missouri | $4,550 | 1.3% |

| Indiana | $4,550 | 1.3% |

| South Dakota | $4,550 | 1.3% |

| Wyoming | $4,550 | 1.3% |

| Oregon | $4,200 | 1.2% |

Tip — always ask your lender for a Loan Estimate document within 3 business days of applying. This legally required document gives you the most accurate closing cost breakdown for your specific loan.

How to reduce your closing costs

While closing costs are largely unavoidable, there are several proven strategies to reduce what you pay. Being proactive before and during the homebuying process can save you thousands of dollars.

Negotiate with your lender

- Ask for a lender credit — some lenders will cover part of your closing costs in exchange for a slightly higher interest rate. This reduces your upfront cash requirement considerably.

- Compare loan estimates — get quotes from at least three lenders. Fees like origination charges and underwriting fees vary widely between lenders and are fully negotiable.

- Request fee waivers — application fees and rate lock fees are often waived if you ask, particularly in a competitive lending environment.

Shop third-party services

- Choose your own title company — you are entitled by law to shop for your own title insurance provider. Prices can vary by hundreds of dollars for the same coverage.

- Schedule your closing at month-end — closing later in the month reduces prepaid interest since it is calculated on a per-day basis from closing date to month end.

- Ask for seller concessions — in many markets, sellers are willing to contribute toward your closing costs as part of the negotiation, especially if the home has been listed for a while.

Learn more from trusted US government resources:

CFPB — What Are Closing Costs? HUD.gov — Buying a Home Guide